How to Buy a Property in Australia (2026): The Step-by-Step Process, From First Chat to Keys

Independent & impartial. We compare 30+ lenders and walk you through every step, from the first chat to the keys.

- The shape of it: the journey runs in three phases, get your borrowing power and pre-approval sorted, buy the property (deposit, contract, conveyancer), then move to unconditional approval and settlement.

- Pre-approval (Approval in Principle) lets you bid at auction or make an offer with confidence, and is typically valid for around 90 days.

- Deposit: the deposit you pay the seller on the day is commonly 10%, though it can be negotiated lower (often 5%). Separately, eligible first home buyers can enter with as little as a 5% deposit and no LMI under the expanded First Home Guarantee.

- Cooling-off: private-sale buyers usually get a short cooling-off period (3 to 5 business days in most states). There is no cooling-off at auction, so finance needs to be sorted before you raise your hand.

- Timeline: from signed contract, formal unconditional approval usually takes up to 14 days, and settlement commonly lands 30 to 90 days later.

- Cost to use a broker: $0, brokers in Australia are paid by the lender at settlement, not by you.

Buying a property is the largest transaction most people ever make, and yet the process itself is rarely laid out plainly. This guide does exactly that: it walks through the whole journey, from the first conversation to the day you collect the keys, in the order it actually happens. You do not need to absorb all of it at once. Think of it as the map, we will focus on the part that is relevant to where you are. Each section opens with a direct answer, then goes deeper.

- What does the buying process actually look like?

- What happens before you start looking?

- What is pre-approval, and how long does it last?

- How much deposit and cash do you really need?

- What happens when you buy, at auction or private sale?

- Do you get a cooling-off period?

- How does the loan reach unconditional approval?

- What happens at settlement?

- What first home buyer schemes can help?

- How does a broker help through all this?

- Glossary of key terms

- Frequently asked questions

What does the buying process actually look like?

It runs in three phases: get finance-ready (borrowing power, then pre-approval), buy the property (deposit, signed contract, conveyancer), and complete the loan (unconditional approval, loan documents, settlement). Pre-approval lasts around 90 days, and settlement is usually 30 to 90 days after you sign.

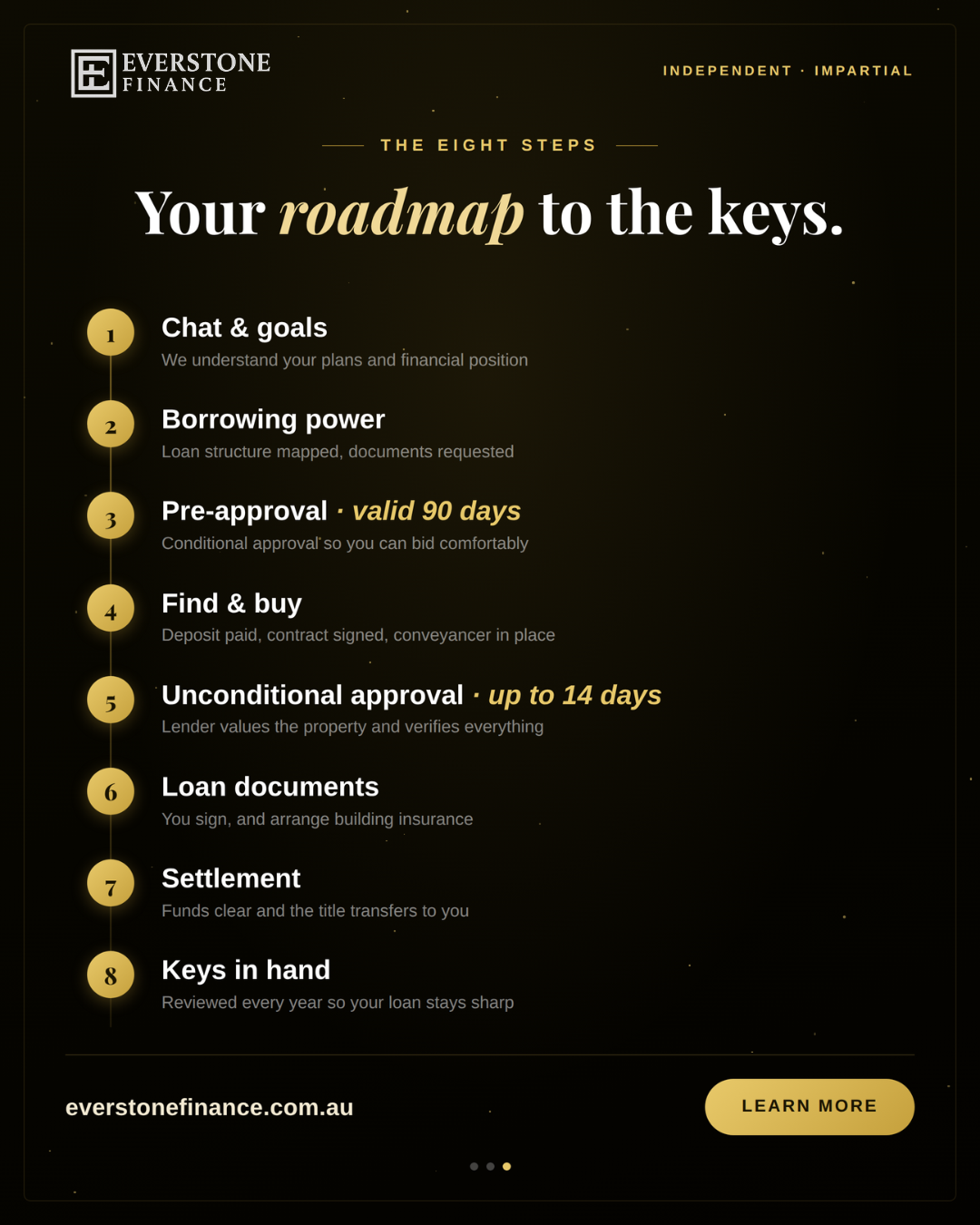

Most purchases follow the same path, whatever the price. Here is the full sequence, end to end:

- 1. Initial conversation. Your goals and financial position are understood, what you want to buy, when, and where you stand today.

- 2. Borrowing power and next steps (about 1 day). Your realistic borrowing capacity and loan structure are mapped, and the documents needed are requested.

- 3. Approval in Principle (up to about 5 days). Your documents are verified and lodged, and the lender issues conditional approval (pre-approval) so you can bid or offer with confidence. It is typically valid for 90 days.

- 4. Purchase of a property. A deposit is paid on the day, a settlement date is agreed, and your solicitor or conveyancer steps in. At auction, finance must already be sorted; on a private sale, a finance clause and cooling-off period may apply.

- 5. Signed contract of sale and any remaining verification documents are provided.

- 6. Formal application for unconditional approval (up to about 14 days). The lender values the property, verifies your documents, and grants formal unconditional approval.

- 7. Loan documents issued. You accept the documents and arrange any remaining items, such as building insurance.

- 8. Funds to complete made available. Your contribution is transferred ready for settlement.

- 9. Settlement completed. Loan accounts appear in your internet banking, and the title transfers from the seller to you.

- 10. Property officially yours, keys received.

- 11. Lending position reviewed annually, so your loan stays competitive long after you move in.

The rest of this guide unpacks the stages that trip people up: pre-approval, the cash you actually need, what happens on purchase day, cooling-off rights, and settlement.

What happens before you start looking?

Two things: a conversation about your goals and financial position, then a clear read on your borrowing power and the right loan structure. This is also when the lender's document checklist is set, so you are ready to move quickly once you find a property.

The first conversation is about understanding where you want to get to and where you are starting from, your income, deposit or equity, existing debts and living costs. From there, your borrowing power can be worked out: not a rough online figure, but a realistic capacity based on how lenders actually assess you, including the buffer rate they apply to repayments.

Just as important is loan structure, the choices that quietly shape the loan for years: fixed versus variable, principal and interest versus interest only, offset accounts, and how the loan is split if you are buying with someone. Getting this right at the start is usually worth more than chasing the lowest advertised rate. You will also be given a clear list of documents to gather, typically payslips, identification, bank statements and details of any existing debts, so nothing holds you up later.

What is pre-approval, and how long does it last?

Pre-approval, also called Approval in Principle or conditional approval, is a lender's confirmation of how much it is willing to lend you, subject to conditions. It lets you bid at auction or make an offer with confidence, and is typically valid for around 90 days.

Once your documents are verified and your consent is given, the lender assesses your application and issues an Approval in Principle. This is not the final, unconditional approval, it is conditional on things like a valuation of the specific property you eventually choose and a final review. But it tells you, and the selling agent, that you are a serious, finance-ready buyer.

Pre-approval usually lasts about 90 days. If you have not bought within that window, it can generally be refreshed. A genuine pre-approval (one the lender has actually assessed, not just a system-generated estimate) is what lets you act decisively when the right place appears, which matters most at auction, where there is no cooling-off period and no finance clause to fall back on.

How much deposit and cash do you really need?

There are two "deposits" to keep separate. The deposit you hand the seller on the day is commonly 10% (often negotiable to 5%). The deposit that decides your loan is your savings as a share of the price: 20% avoids LMI normally, but eligible first home buyers can start with just 5% and no LMI. On top of the deposit, budget for stamp duty, legal and inspection costs.

This is where many buyers get caught out, because the word "deposit" is used two ways. The deposit paid to the seller on signing or at the fall of the hammer is commonly 10% of the purchase price, though it can be negotiated lower, sometimes 5%, particularly in a private sale arranged in advance. The deposit that drives your loan is your own funds as a percentage of the price: 20% is the level that normally avoids Lenders Mortgage Insurance, while government support and select lender policies can let you buy with far less.

Beyond the deposit, the other upfront cost to plan for is stamp duty (transfer duty), which varies by state and by whether you qualify for a first home buyer concession or exemption. Then there are smaller but real costs: conveyancing or legal fees, building and pest inspection, loan and government registration fees, and building insurance from settlement. A good rule of thumb is to budget for these alongside the deposit rather than as an afterthought, because they decide how much you genuinely need in the bank.

What happens when you buy, at auction or private sale?

When your offer is accepted or you win at auction, you sign the contract of sale, pay the deposit, and a settlement date is agreed. How much protection you have depends on the method: auctions are unconditional with no cooling-off and no finance clause, while private sales often allow a finance clause and a cooling-off period.

At an auction, the sale is binding the moment the hammer falls. You pay the deposit on the spot, there is no cooling-off period, and you cannot make the contract conditional on finance. That is precisely why finance and a building and pest inspection should be sorted before you bid.

In a private sale (private treaty), there is more room to manage risk. You can often negotiate a finance clause (making the contract conditional on your loan being formally approved), arrange inspections after signing, and rely on the statutory cooling-off period in your state. In both cases, your solicitor or conveyancer should review the contract, and in some states the vendor's disclosure statement (a Section 32 in Victoria, a Form 1 in South Australia), before you commit.

Before you sign or bid: have your pre-approval in place, your conveyancer briefed, and your building and pest inspection booked. The smartest move is to time the inspection so the report lands at the start of any cooling-off period, not at the end of it.

Do you get a cooling-off period?

Usually yes for a private sale, and no for an auction. A cooling-off period is a short window after signing in which you can withdraw, generally for a small penalty. It runs from 0 to 5 business days depending on the state, and every state removes it for auction purchases.

Cooling-off rights are set by each state and territory, and they differ more than most buyers expect. They are a safety net for private-treaty purchases, a few business days to confirm finance, complete inspections and have your conveyancer finish their checks. Crucially, cooling-off does not apply when you buy at auction (and in some states, not in the days immediately around a scheduled auction either). Here is the snapshot:

| State / Territory | Cooling-off period | Withdrawal penalty |

|---|---|---|

| NSW | 5 business days | 0.25% of the price |

| VIC | 3 clear business days | 0.2% of the price (or $100, whichever is greater) |

| QLD | 5 business days | 0.25% of the price |

| SA | 2 clear business days | Varies (deposit may be refundable) |

| ACT | 5 business days | 0.25% of the price |

| NT | 4 business days | Generally refunded in full |

| WA | None (statutory) | Protection comes via contract conditions instead |

| TAS | None (statutory) | Protection comes via contract conditions instead |

Because the rules vary so much, the practical takeaway is the same everywhere: do not rely on cooling-off as your plan, treat it as a backstop. Have finance and inspections lined up first, especially in WA and Tasmania, where there is no statutory period at all.

How does the loan reach unconditional approval?

Once you have a signed contract, the formal application goes in. The lender orders a valuation of the property, verifies all your documents, and then issues unconditional (formal) approval. This usually takes up to about 14 days.

With the contract signed, the loan moves from conditional to formal. Two things happen in parallel: the lender verifies your documents in full, and it orders a valuation of the property to confirm the price is in line with market value. Once both are satisfied, you receive unconditional approval, the green light that the loan will proceed.

A valuation can come in lower than the price you paid, known as a valuation shortfall. If it does, the lender bases your loan on the lower figure, which can mean finding extra cash or restructuring. This risk is highest at auction, where you commit before a lender valuation, and it is one more reason to have your finance assessed properly beforehand.

Timeframes are a guide, not a guarantee. Valuations, document turnaround and lender workloads all affect the pace. Building a sensible buffer into your settlement date protects you.

What happens at settlement?

You accept the loan documents, arrange building insurance, and transfer your contribution (the funds to complete). On the agreed settlement date, the money changes hands, the title transfers from the seller to you, and the keys are released.

After unconditional approval, the lender issues your loan documents. You review and accept them, and put any final items in place, most commonly building insurance, which lenders require from the settlement date. Your funds to complete (your deposit balance plus costs, less any deposit already paid) are then transferred ready for the day.

On settlement day, your lender and conveyancer coordinate with the seller's side to exchange funds and documents, increasingly through electronic settlement. When it completes, the Transfer of Land is registered, the title moves into your name, your loan accounts appear in your internet banking, and the agent releases the keys. The property is officially yours.

The job is not quite finished, though. A good broker reviews your lending position each year, checking your rate against the market and handling a switch if a sharper deal appears, so the loan keeps working for you long after move-in.

Sources and useful references

Walk through your purchase, free

Book a no-obligation chat and we will map your borrowing power, the deposit you need, and the exact steps for your situation, in plain English.

Book an appointmentWhat first home buyer schemes can help?

The biggest is the First Home Guarantee. Since 1 October 2025 it has been expanded: unlimited places, no income caps, and higher property price caps. It lets eligible first home buyers purchase with a 5% deposit and no LMI, with the government guaranteeing the rest. State grants and stamp duty concessions can apply on top.

If you are buying your first home, the support available changed significantly in late 2025. The First Home Guarantee now has no limit on places, no income caps, and raised price caps, opening it to far more buyers. Under it, the government acts as guarantor for the gap between your deposit and 20%, so an eligible buyer can enter with a 5% deposit and avoid Lenders Mortgage Insurance entirely, a saving that can run into the tens of thousands. The main constraint now is the property price cap for your area:

| Location | Price cap |

|---|---|

| Sydney & NSW regional centres | $1,500,000 |

| Brisbane & QLD regional centres | $1,000,000 |

| Melbourne & Geelong | $950,000 |

| Adelaide | $900,000 |

| Perth | $850,000 |

On top of the Guarantee, most states offer a First Home Owner Grant and stamp duty concessions or exemptions for eligible buyers, which vary by state and price. We have pulled the full national picture together in our companion guide, First Home Buyers in Australia 2026: every grant, scheme and stamp duty saving by state. Eligibility rules apply to all of these, and the right combination depends on your situation, which is exactly what a broker can confirm for you.

How does a broker help through all this?

A broker runs the process for you end to end: working out your true borrowing power, structuring the loan, securing pre-approval, comparing lenders to match your goals, and managing the application through to settlement, then reviewing it each year. In Australia the broker is paid by the lender, so there is no cost to you.

A single bank can only show you its own products and its own rules. A broker compares across the market, finds the lender whose policy and pricing genuinely fit your deposit, income and plans, and then does the heavy lifting: the paperwork, the lender liaison, the timing around your contract and settlement dates, and the problem-solving when something needs sorting quickly.

At Everstone Finance, we are independent and impartial. We compare more than 30 lenders, we are paid by the lender (not by you), and we explain every step in plain English so you always know what is happening and why. Founded by ex-bankers, we know how lenders assess and price loans from the inside, and we stay with you after settlement, reviewing your position every year so your loan keeps working for you.

Glossary of key terms

- Pre-approval (Approval in Principle)

- A lender's conditional confirmation of how much it will lend you, subject to a valuation and final checks. Lets you bid or offer with confidence, and typically lasts around 90 days.

- Unconditional (formal) approval

- Final approval after the lender has valued the property and verified your documents. The loan will proceed.

- Borrowing power

- The realistic amount a lender will lend you, based on income, expenses, debts and an assessment buffer, not just an online estimate.

- Cooling-off period

- A short window after signing a private-sale contract in which you can withdraw, usually for a small penalty. It varies by state and does not apply at auction.

- Finance clause

- A condition in a private-sale contract that lets you exit without penalty if your loan is not formally approved. Not available at auction.

- Lenders Mortgage Insurance (LMI)

- A one-off premium normally charged when you borrow more than 80% of a property's value. It protects the lender, not you. Schemes and certain policies can waive it.

- Valuation shortfall

- When the lender's valuation comes in below the price you paid, so the loan is based on the lower figure. May require extra funds.

- Settlement

- The day funds and documents are exchanged, the title transfers to you, and the keys are released.

- Conveyancer / solicitor

- The professional who reviews the contract and vendor disclosure, conducts searches, and manages the legal side through to settlement.

- First Home Guarantee

- A government scheme letting eligible first home buyers purchase with a 5% deposit and no LMI. Since 1 October 2025: unlimited places, no income caps, higher price caps.

Frequently asked questions about buying a property

How long does it take to buy a property in Australia?

From a finance-ready start, pre-approval takes up to about 5 days, then once you have a signed contract, formal unconditional approval usually takes up to 14 days, with settlement commonly 30 to 90 days after signing. The whole journey can run from a few weeks to a couple of months, depending on how quickly you find a property and your settlement terms.

How much deposit do I need to buy a property?

Two figures matter. The deposit paid to the seller on the day is commonly 10%, though it can be negotiated lower (often 5%). Separately, the deposit that drives your loan is your savings as a share of the price: 20% normally avoids LMI, but eligible first home buyers can start with as little as 5% and no LMI under the First Home Guarantee. Remember to also budget for stamp duty, legal and inspection costs.

What is the difference between pre-approval and unconditional approval?

Pre-approval (Approval in Principle) is conditional: the lender confirms how much it will lend, subject to valuing your chosen property and final checks. Unconditional approval is the final green light, granted after the lender has valued the property and verified everything. You generally need pre-approval before bidding and unconditional approval after signing a contract.

Do I get a cooling-off period when I buy?

Usually yes for a private sale, and no for an auction. Cooling-off periods run from 0 to 5 business days depending on the state (for example, 5 in NSW and QLD, 3 in VIC), generally with a small penalty if you withdraw. Every state removes cooling-off for auction purchases, which is why finance should be sorted before you bid.

What happens at settlement?

You accept your loan documents, arrange building insurance and transfer your funds to complete. On the agreed date, your lender and conveyancer exchange funds and documents with the seller's side, the Transfer of Land is registered, the title moves into your name, and the keys are released. The property is then officially yours.

Can a valuation come in lower than the purchase price?

Yes. This is a valuation shortfall: if the lender values the property below the price you paid, the loan is based on the lower figure, which can mean contributing extra funds. The risk is highest at auction, where you commit before a lender valuation, so getting your finance assessed properly beforehand matters.

Can first home buyers really buy with a 5% deposit and no LMI?

Yes, if eligible. The First Home Guarantee lets eligible first home buyers purchase with a 5% deposit and no Lenders Mortgage Insurance, with the government guaranteeing the gap. Since 1 October 2025 it has unlimited places, no income caps and higher price caps (for example, up to $1.5 million in Sydney and $950,000 in Melbourne). Price caps and other eligibility rules apply.

Does it cost anything to use a mortgage broker?

No. Mortgage brokers in Australia are paid by the lender at settlement, not by you, so there is no cost to you for the advice. Using a broker also means comparing many lenders rather than seeing just one bank's products and rules.

Do I need to be in Melbourne or South Yarra to work with Everstone Finance?

No. Everstone Finance is based in South Yarra and meets locally in person, but works with buyers across Melbourne and Australia-wide by phone and Zoom.

The bottom line: buying a property is really three phases, get finance-ready, buy well, then complete the loan and settle. Know your borrowing power and pre-approval before you look, understand the deposit and costs, and have your finance and inspections sorted before you bid (especially at auction, where there is no cooling-off). Get an independent review before you commit.

Talk to an independent broker, free

No cost, no obligation. We compare 30+ lenders and walk you through your purchase step by step, from borrowing power to settlement.

Book an appointment