10 Questions to Ask a Mortgage Broker Before You Commit (2026)

Independent & impartial. A great broker welcomes every one of these questions, and is always glad to answer them.

- A broker is free to you. In Australia the lender pays the broker, not you, and that commission is disclosed in writing before your loan is submitted.

- Little incentive to steer you. Since the Royal Commission, lender commissions are broadly similar, so the stronger incentive is simply to find your best fit.

- The law is on your side. Brokers are bound by a Best Interests Duty to put your interests first, a standard a bank's own staff are not held to.

- What good looks like. A strong broker compares at least three lenders, explains the comparison rate (not just the headline rate), and gives you the recommendation in writing.

A mortgage is the biggest financial commitment most people ever make, so the person arranging it matters. The questions below are the fastest way to tell a broker who genuinely works for you from one who simply sells what is in front of them. A great broker welcomes every one of them. Each question opens with a direct answer, the way we would answer it at Everstone Finance, then goes a little deeper.

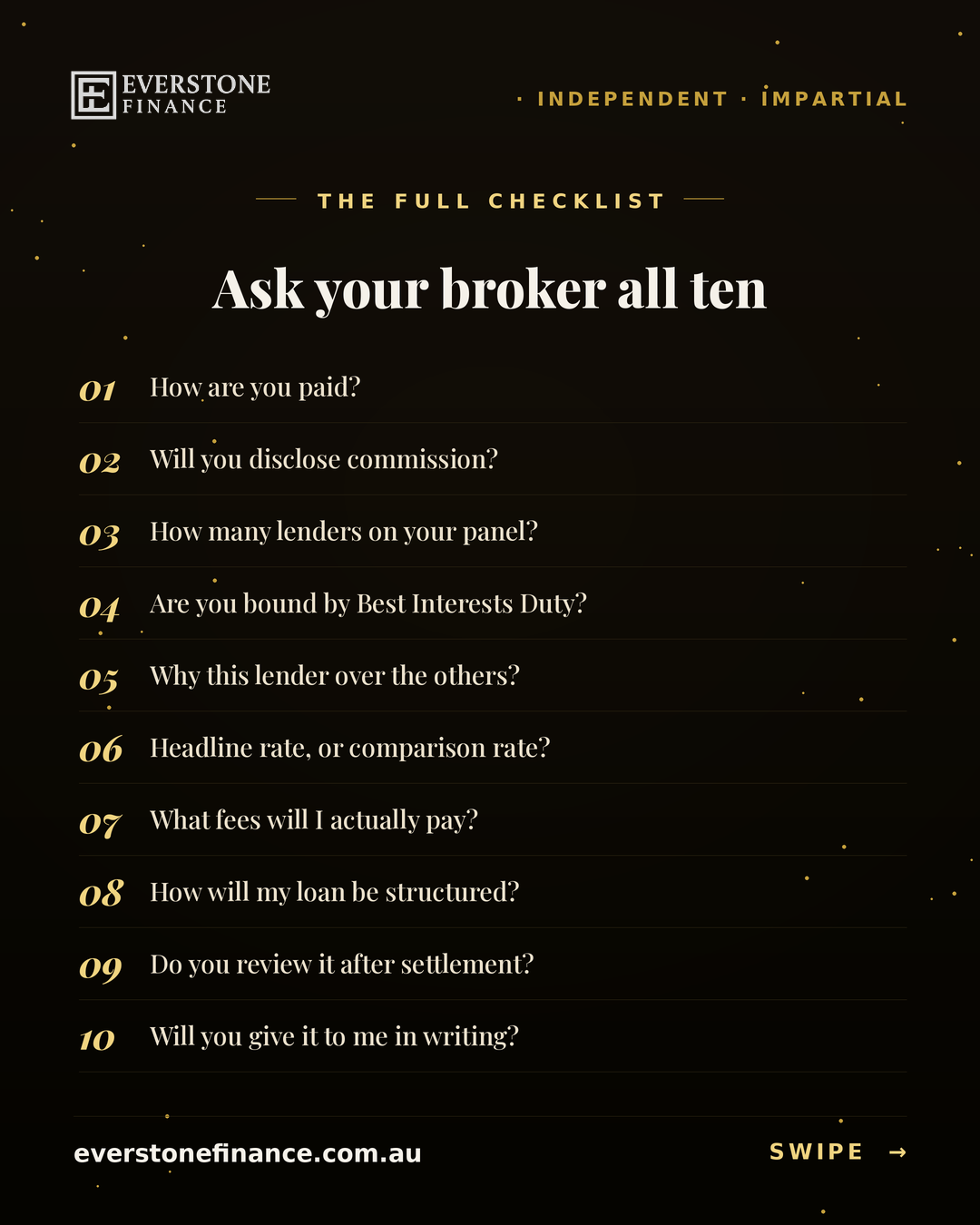

- How many lenders are on your panel?

- How are you paid, and will you disclose it?

- Are you bound by the Best Interests Duty?

- Why this lender over the others?

- Headline rate, or comparison rate?

- What fees will I actually pay?

- How should my loan be structured?

- What happens after settlement?

- What are your credentials?

- Will you give it to me in writing?

How many lenders are on your panel, and which ones?

Enough to shop the whole market for you. A strong panel covers all the major banks plus a range of second-tier and specialist lenders, around 30 or more, so the recommendation can be matched to your situation rather than limited to a short list.

This question checks whether the broker can compare the market or only a narrow slice of it. A broker tied to a handful of lenders can only ever recommend from that handful. A broad panel covers the majors, so your everyday lending needs are met, plus specialist lenders for situations that fall outside the ordinary, such as self-employed income, recent visa holders, niche property types or credit history that needs a more flexible assessor.

Ask for a number. "All the major lenders" is reassuring, but "a panel of 30-plus lenders including all four majors" is verifiable. Specifics signal a broker who knows their own panel.

How are you paid, and will you disclose your commission?

The lender pays the broker, not you, so the service is free to you. Payment comes as an upfront commission (a percentage of the loan, paid at settlement) and a smaller trail commission (paid while the loan stays with that lender). Both are disclosed in writing before your loan is submitted, and neither adds anything to your rate or repayments.

This is the single most important question, and a good broker answers it without flinching. The bank pays a broker to place and manage the loan because it is cheaper for them than acquiring and servicing the customer directly. You should receive these figures in writing, in a Credit Proposal Disclosure document, before your loan is lodged, not buried in fine print afterwards.

Why it matters: since the 2019 Royal Commission, commission structures were reformed and are now broadly similar across lenders. That removes most of the financial reason to push you toward one bank, so the stronger incentive is simply to find your best fit.

Are you bound by the Best Interests Duty, and how do you apply it?

Yes. Since 2021, mortgage brokers in Australia have been bound by a legal Best Interests Duty to act in the client's best interests and put them ahead of the broker's own. A bank's own staff are not held to this same duty, which is a real structural advantage of using a broker.

The more revealing half of the question is how they apply it. A good broker can describe it in practice: assessing your goals first, comparing genuinely competitive options, and being able to justify, in writing, why the recommended loan suits you better than the alternatives. When commissions are broadly level anyway, applying the duty is not a sacrifice, it is simply the job.

What's your recommendation, and why this lender over the others?

The recommendation should start with your goals, not the lender's brochure. If your priority is the lowest rate, the broker points to the lender sharpest on rate for your profile; if you value a strong app and self-service, that is a different recommendation; if your situation is unusual, it reflects which lender's credit team handles that scenario best.

That tailoring is the entire value of a broker. Experience across many lenders and many client situations is what lets them map your scenario to the lender most likely to say yes on the best terms. A good answer reasons from your circumstances; a weak one names a default they hand everyone.

Are you quoting the headline rate, or the comparison rate?

The headline rate is the advertised interest rate before fees. The comparison rate folds the rate together with most fees into a single figure, so you can compare loans like for like. A low headline rate attached to high fees can cost more than a slightly higher rate with none.

As we put it to clients, the headline rate lets you compare apples with strawberries; the comparison rate lets you compare apples with apples. Always ask for the comparison rate, and ask the broker to show you the fee breakdown behind it.

What fees will I actually pay, to you and on the loan?

With most brokers there are no fees to you, the lender pays them. Separately, the loan itself may carry lender fees: application or establishment, valuation, ongoing or annual package fees, and a discharge fee when you leave. A good broker lays these out alongside the rate and looks for lenders who waive or minimise them where it suits your plan.

Confirm the "free to you" point directly, because a small number of brokers do charge a fee in certain situations. Then make sure the loan's own costs are on the table, so the comparison between options is honest rather than flattering to one product.

How should my loan be structured for my situation?

Structure can matter as much as rate. A good broker walks you through fixed versus variable, principal and interest versus interest only, a linked offset account, redraw, and extra repayments, then tailors the mix to your goals rather than selling a default product.

Fixed vs variable. A fixed loan locks your rate for a set term, usually one to five years, so repayments do not move regardless of the market. A variable loan moves with the market. Many borrowers split across both.

Offset and redraw. A linked offset account is a transaction or savings account attached to your loan. The lender calculates the balance daily and subtracts it from your loan before working out interest, so money in offset directly reduces the interest you pay, which is charged monthly. Redraw works to similar effect by letting you pull back extra repayments you have made.

Worth knowing: features are evolving, and some lenders now offer offset accounts even on fixed loans, usually with conditions. That is exactly the kind of detail a broker stays across so you do not have to. For the bigger picture, see our step-by-step guide to buying a property in Australia.

What happens after settlement, and do you review my loan?

The relationship should not end at settlement. A good broker reviews your lending periodically, we do it annually, which is enough time for the market to shift and for any meaningful saving to surface. At review you can see how your rate compares and decide whether to renegotiate or refinance.

Review cadence varies between brokers, so it is fair to ask what theirs is. A broker who disappears once they have been paid is a different proposition from one who keeps your loan competitive year after year.

What are your credentials and track record?

Look for membership of an industry body, the FBAA or MFAA, which carries conduct and education standards. Then ask about background and tenure. Time inside a major bank gives a broker a working understanding of how credit decisions are actually made.

At Everstone, that includes 8+ years at NAB, one of Australia's big four, across multiple roles, a Master's in Business, and a Bachelor's in Engineering, a background that brings a structured, problem-solving approach to complex scenarios. Genuine reviews and a record of settling loans like yours round out the picture.

Will you give me the recommendation and comparisons in writing?

The answer should be an unqualified yes. A good broker presents the options available to you, typically comparing at least three lenders with their different offers, says which they would choose and why, then leaves the decision entirely with you, on the record.

Having it in writing lets you compare calmly in your own time and keeps a clear record of the advice you were given. If a broker prefers to keep the recommendation verbal, treat that as your answer.

Sources and useful references

Ask us all ten, free

Book a no-obligation chat and we will answer every one of these questions for your situation, clearly and in plain English, with your goals first.

Book an appointmentGlossary of key terms

- Lender panel

- The banks and lenders a broker is accredited to write loans with. A wider panel means more options for your situation.

- Upfront commission

- A percentage of your loan amount the lender pays the broker at settlement. Paid by the lender, not by you.

- Trail commission

- A smaller ongoing percentage the lender pays the broker for as long as the loan stays with that lender. Also paid by the lender, not by you.

- Best Interests Duty

- A legal obligation, in force since 2021, requiring mortgage brokers to act in the client's best interests and put them ahead of the broker's own.

- Headline rate

- The advertised interest rate, before fees.

- Comparison rate

- The interest rate plus most fees expressed as a single figure, so loans can be compared like for like.

- Offset account

- A linked account whose balance is subtracted from your loan balance before interest is calculated daily, reducing the interest you pay.

- Redraw

- A facility that lets you access extra repayments you have already made on a variable loan.

Frequently asked questions

Does a mortgage broker cost me anything?

For most borrowers, no. The lender pays the broker through commission at settlement, so the service is free to you. A small number of brokers charge a fee in certain situations, so it is worth confirming directly before you start.

Will a mortgage broker just send me to whichever bank pays them the most?

Since the Royal Commission, lender commissions are broadly similar, so there is little financial reason to favour one bank. Brokers are also legally bound by the Best Interests Duty to recommend what suits you, and a good broker discloses their commissions in writing before submitting your loan.

What is the difference between the headline rate and the comparison rate?

The headline rate is the advertised interest rate before fees. The comparison rate combines the rate with most fees into a single figure so you can compare loans like for like. A low headline rate with high fees can cost more than a slightly higher rate with none.

How many lenders should a mortgage broker compare for me?

A good broker typically compares at least three lenders, presents the different offers, recommends the one they believe best suits your goals and explains why, then leaves the decision to you in writing.

What is an offset account and how does it work?

An offset account is a linked transaction or savings account. The lender calculates its balance daily and subtracts it from your loan balance before working out interest, so money held in offset reduces the interest you pay. Some lenders now offer offset even on fixed loans, usually with conditions.

Is a mortgage broker bound to act in my best interests?

Yes. Since 2021, mortgage brokers in Australia have been bound by a Best Interests Duty, a legal obligation to act in the client's best interests and put them ahead of the broker's own. A bank's own staff are not held to that same duty.

Does a mortgage broker review my loan after settlement?

A good one does. At Everstone we review lending annually, enough time for the market to move and for any worthwhile saving to surface, so you can see how your rate compares and decide whether to renegotiate or refinance. Review frequency varies between brokers, so it is fair to ask.

Do I need to be in Melbourne or South Yarra to work with Everstone Finance?

No. Everstone Finance is based in South Yarra and meets locally in person, but works with clients across Melbourne and Australia-wide by phone and Zoom.

The bottom line: a great broker welcomes scrutiny. Ask how they are paid and whether they will disclose it, how wide their panel is, whether they apply the Best Interests Duty, how they would structure your loan and why, and whether you will get it all in writing. At Everstone, the answer to all ten is yes.

Talk to an independent broker, free

No cost, no obligation. We compare 30+ lenders and answer all ten questions for your situation, clearly and in writing.

Book an appointment