Still Waiting for 3% Mortgage Rates? 50 Years of Australian History Says Don't (2026)

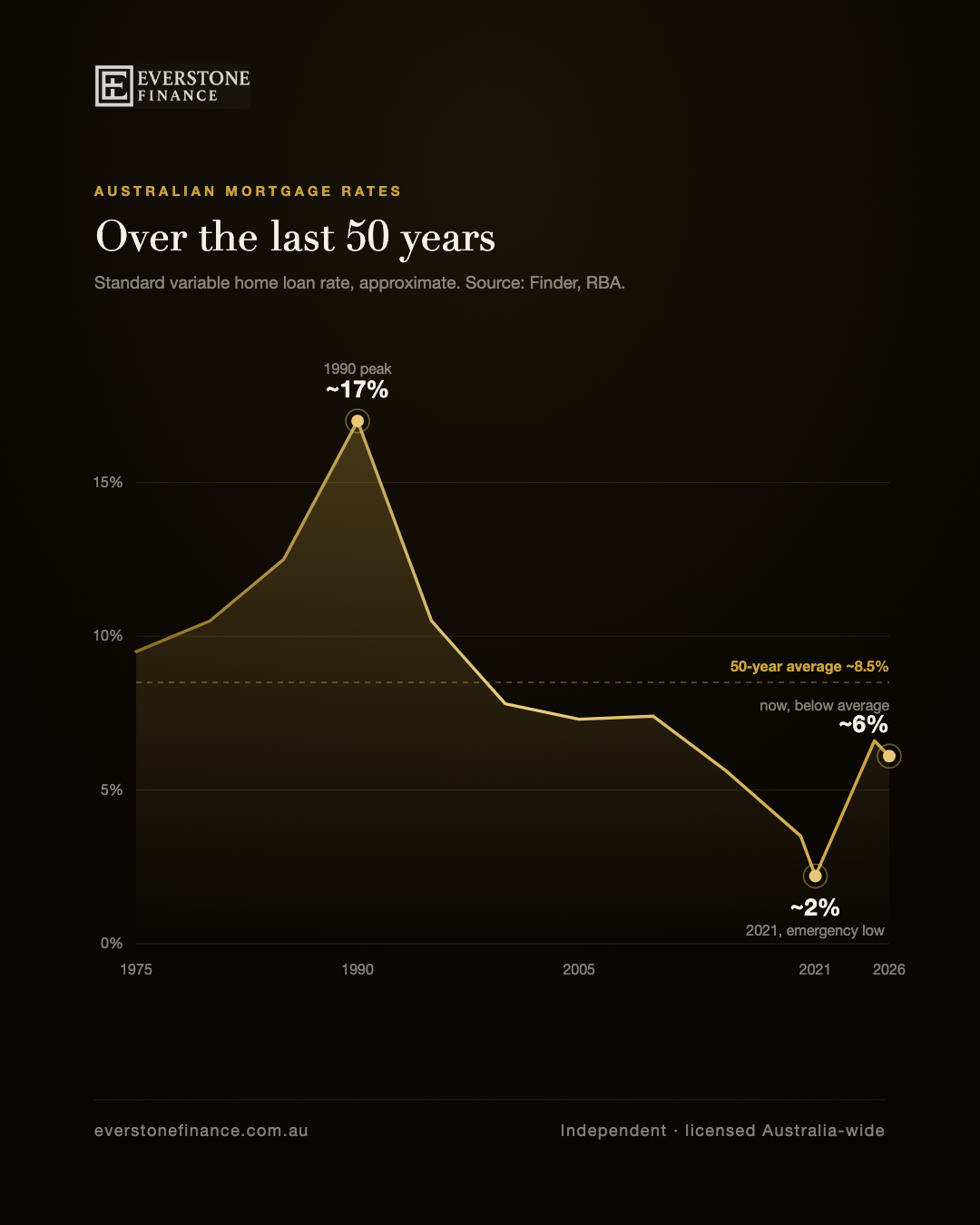

Australian standard variable home loan rate, approximate, 1975 to 2026. Sources: Finder, RBA, MPA. The 1990 peak near 17 percent, the 2021 low near 2.2 percent, and today near 6 percent.

In January 1990, the standard Australian variable home loan rate hit roughly 17 percent. Your parents paid it. Today you are looking at about 6 percent and calling it high, and waiting for 3 percent to come back. Here is the uncomfortable truth: across 50 years of Australian rate history, the average sits near 8 to 9 percent. Today's rate is below the long run average. The 2 percent of 2020 and 2021 was not the baseline you missed out on, it was an emergency setting, a glitch that has appeared only once in half a century. This is the long view on where rates have actually been, and why "waiting for 3 percent" is a decision that can quietly cost you the house. Figures here are approximate, indicative and historical, and this is general information rather than financial advice.

- The all-time peak for the Australian standard variable rate was roughly 17 percent in January 1990. To a generation of borrowers, that was simply the going rate.

- The 50-year average standard variable rate is roughly 8 to 9 percent, so today's approximately 6 percent sits below the long-run average, not above it. These are indicative, historical figures.

- The record low near 2.2 percent in 2021 came from the RBA cutting the cash rate to 0.10 percent during the pandemic, an emergency setting, not a normal baseline. Rates that low have appeared only once in 50 years.

- As of mid 2026 the RBA is on hold. Economists are split: some see a cut ahead, others read trimmed mean inflation near 3.6 percent and unemployment at 4.4 percent as reason to stay put or even hike. We are not forecasters and do not promise where rates go.

- You cannot move the RBA, but a broker comparing a panel of over 40 bank and non-bank lenders, licensed Australia-wide, can move the rate you personally pay, and refinance it again when the cycle turns.

- Is 6% high for a mortgage rate in Australia, historically?

- Will mortgage rates go back to 3%? Why the 2% era was the glitch, not the goal

- When will the RBA cut rates? Why nobody can reliably time it

- Should I wait for rates to drop before buying? The real cost of waiting

- What does "date the rate, marry the house" mean?

- Can a broker actually get me a lower rate? The one lever you control

- FAQ

Is 6% high for a mortgage rate in Australia, historically?

No. Across 50 years of Australian home loan history, the standard variable rate has averaged roughly 8 to 9 percent. Today's approximately 6 percent sits below that long-run average. The rate peaked near 17 percent in 1990 and only dipped near 2.2 percent during the pandemic emergency. These figures are approximate and historical.

Here is the 50-year picture of the Australian standard variable home loan rate, approximate and historical, in roughly five-year steps. These are indicative figures sourced to Finder, the RBA and MPA, and they are the cleanest way to see where 6 percent actually sits.

- 1975: about 9.5%

- 1980: about 10.5%

- 1985: about 12.5%

- 1990: about 17.0% (the all-time peak, January 1990)

- 1995: about 10.5%

- 2000: about 7.8%

- 2005: about 7.3%

- 2010: about 7.4%

- 2015: about 5.6%

- 2020: about 3.5%

- 2021: about 2.2% (the record low)

- 2025: about 6.6%

- 2026: about 6.1%

Read that column top to bottom and the framing changes. Across most of that history, a 6 in front of your rate would have been a good day. The number that feels painful today would have looked like relief to a borrower in 1990, and ordinary to a borrower in 2005. Six percent is not the ceiling. On the long view it is below the middle.

Will mortgage rates go back to 3%? Why the 2% era was the glitch, not the goal

Probably not as a normal setting. The roughly 2 percent rates of 2020 and 2021 existed because the RBA cut the cash rate to 0.10 percent to support the economy through the pandemic. That was an emergency lever, an anomaly that has appeared only once in 50 years, not the baseline rates are meant to return to. We do not forecast where rates go.

It is worth being honest about what happened. The sub-3 percent era was not the reward for patience. It was an emergency. When the RBA pushed the cash rate to 0.10 percent, it was doing crisis economics, the way a defibrillator is not how a healthy heart is meant to beat. Rates that low have appeared exactly once in 50 years of Australian history, and they appeared because something was badly wrong.

So when the goalpost in your head is 3 percent, you have quietly anchored your entire buying decision to the single most abnormal moment in half a century of data. Everything else, the 7s of the 2000s, the 5s of the 2010s, today's 6, looks expensive only by comparison to a number that was never normal. Move the anchor back to where the data actually lives, the 8 to 9 percent long-run average, and today's rate stops looking like a problem and starts looking like a window.

When will the RBA cut rates? Why nobody can reliably time it

As of mid 2026, the RBA is on hold and the experts disagree. NAB's Alan Oster has the cash rate holding before easing, while others read trimmed mean inflation near 3.6 percent and unemployment at 4.4 percent as hawkish, and price some chance of a hike. We are not forecasters and do not promise where rates go.

If the professionals who do this for a living cannot agree on direction, the idea that you will personally time the bottom of the cycle is optimistic. One credible economist sees a cut coming. Another looks at the same inflation and jobs data and sees reasons to stay on hold, or even tighten. Both are reading real numbers. Both could be right depending on the data that lands next.

That disagreement is the point. Trying to time the RBA is a fool's errand, not because the people doing it are foolish, but because the system is genuinely uncertain and nobody owns a crystal ball, including us. We do not promise where rates go. What we can tell you is that a buying or refinancing decision built on correctly guessing the RBA is a decision built on the one variable you have the least control over.

Should I wait for rates to drop before buying? The real cost of waiting

Waiting has a price most people never add up. While you hold out for a cut that may never bring back 3 percent, property prices keep moving and you keep paying rent. Trying to save 0.25 percent while the market runs is often a losing trade, because the saving is small and the cost of delay is not. This is general information, not financial advice.

Make it concrete. A 0.25 percent rate cut on a 600,000 dollar loan is real money, but it is a modest monthly figure. Now put it next to a market that moves a few percent a year. If prices rise even 5 percent on an 800,000 dollar home while you wait, that is 40,000 dollars of entry price, and it dwarfs the repayment saving you were holding out for. You can see exactly how repayments differ city by city in our breakdown of monthly mortgage repayments across Australian cities, which makes the price-versus-waiting maths hard to ignore.

And every month spent waiting is a month of rent, money that buys you no equity and disappears entirely. This is loss aversion working against you in the worst way: the fear of buying at the wrong rate feels vivid and urgent, while the slow, quiet cost of rent and rising prices barely registers, until you tally a full year of it. Inaction is not the safe, neutral choice it feels like. It is a position, and it has a cost.

What does "date the rate, marry the house" mean?

It means you commit to the home, not the interest rate. Buy the right property when you are ready and able, because that is the long-term decision. The rate is temporary: you can refinance it down when the cycle turns. You marry the house. You only date the rate.

The phrase reframes the whole decision. People freeze because they treat the rate as permanent, as if signing today locks them into 6 percent forever. It does not. Your loan is not a marriage to a number. It is a relationship you can renegotiate. When the cycle turns and rates ease, you refinance, and the rate you were so afraid of becomes a footnote.

The house is the part that is hard to get back. The right property, in the right area, at today's price, is a long-term decision. The rate attached to it on day one is an adjustable variable. So separate them. Make the big, durable decision, the home, on its own merits, and treat the rate as the adjustable thing it actually is. When you are ready to switch, our complete refinance guide walks through exactly how to move your loan to a sharper rate, and if you are not sure where your current rate even stands, the home loan self-audit shows you whether you are overpaying right now.

Can a broker actually get me a lower rate? The one lever you control

Yes. You cannot move the RBA, but the rate you personally pay is not fixed by the cash rate alone. As an independent broker comparing a panel of over 40 bank and non-bank lenders, licensed Australia-wide, we can find a sharper rate for your situation, then refinance it again when the cycle turns. Eligibility and lender criteria apply.

Here is the lever nobody talks about while they wait for the RBA. The cash rate sets the weather, but the rate you actually pay depends on your lender, your loan structure, your equity and how hard someone shops it. Two borrowers with identical incomes can pay materially different rates simply because one settled and one compared. That gap is yours to capture, regardless of what the RBA does next.

That is the whole Everstone proposition. We are independent, licensed Australia-wide (Credit Representative 526374, Australian Credit Licence 391237), and our advice is free because the lender pays us, not you. We compare a panel of over 40 bank and non-bank lenders to find your sharpest rate now, and we are on hand to refinance it down when the cycle turns. Eligibility and lender criteria apply, and any rates quoted are indicative. Stop trying to control the one thing you cannot, the RBA, and pull the one lever you can. Book an appointment with Ahmed and we will review your rate.

Stop waiting. Sharpen the rate you can actually control.

You cannot move the RBA, but we can test your rate against a panel of over 40 bank and non-bank lenders, today, and refinance it again when the cycle turns. Book a rate review and we will run your numbers. No cost, no obligation, anywhere in Australia.

Book an appointmentFrequently asked questions

Will Australian mortgage rates go back to 3%?

It is unlikely as a normal setting. Rates near 2 to 3 percent appeared in 2020 and 2021 because the RBA cut the cash rate to 0.10 percent as an emergency response to the pandemic. In 50 years of Australian history, rates that low have happened only once. The long-run average sits closer to 8 to 9 percent. We are not forecasters and do not promise where rates go, but anchoring your decision to 3 percent means anchoring it to the most abnormal moment in half a century. These figures are approximate and historical.

Is 6 percent a high mortgage rate in Australia historically?

No. The standard variable rate has averaged roughly 8 to 9 percent over the past 50 years. It peaked near 17 percent in January 1990 and sat in the 7s through much of the 2000s. Today's approximately 6 percent is below the long-run average. These figures are indicative and historical, sourced to Finder, the RBA and MPA.

Should I wait for rates to drop before buying a home?

Waiting carries a cost that is easy to miss. While you hold out for a cut that may never restore 3 percent, property prices can keep rising and rent keeps leaving your pocket with nothing to show for it. A 0.25 percent rate saving is often small next to a few percent of price growth on the home you wanted. This is general information, not financial advice, but the cost of inaction is real and worth adding up.

What does 'date the rate, marry the house' mean?

It means commit to the property, not the interest rate. Buy the right home when you are ready, because that is the durable, long-term decision. The rate is temporary and adjustable: you can refinance it lower when the cycle turns. You marry the house and only date the rate.

When will the RBA cut interest rates?

Nobody knows reliably. As of mid 2026 the RBA is on hold and economists are split. NAB's Alan Oster has the cash rate holding before easing, while others read trimmed mean inflation near 3.6 percent and unemployment at 4.4 percent as reasons to stay put or even hike. We do not forecast rates, and the disagreement among experts is exactly why trying to time the RBA is so difficult.

Can a mortgage broker get me a lower rate?

A broker can compare lenders to find a sharper rate for your specific situation, which is the part of your rate you can actually influence. Everstone is independent and compares a panel of over 40 bank and non-bank lenders, licensed Australia-wide (Credit Representative 526374, Australian Credit Licence 391237). Our advice is free because the lender pays us. Eligibility and lender criteria apply, and rates quoted are indicative.