World-Class Football, World-Class House Prices: Four Australian Cities Among the World’s Least Affordable (2026)

Median home price vs household income across the world’s least affordable cities (Forbes, 2026).

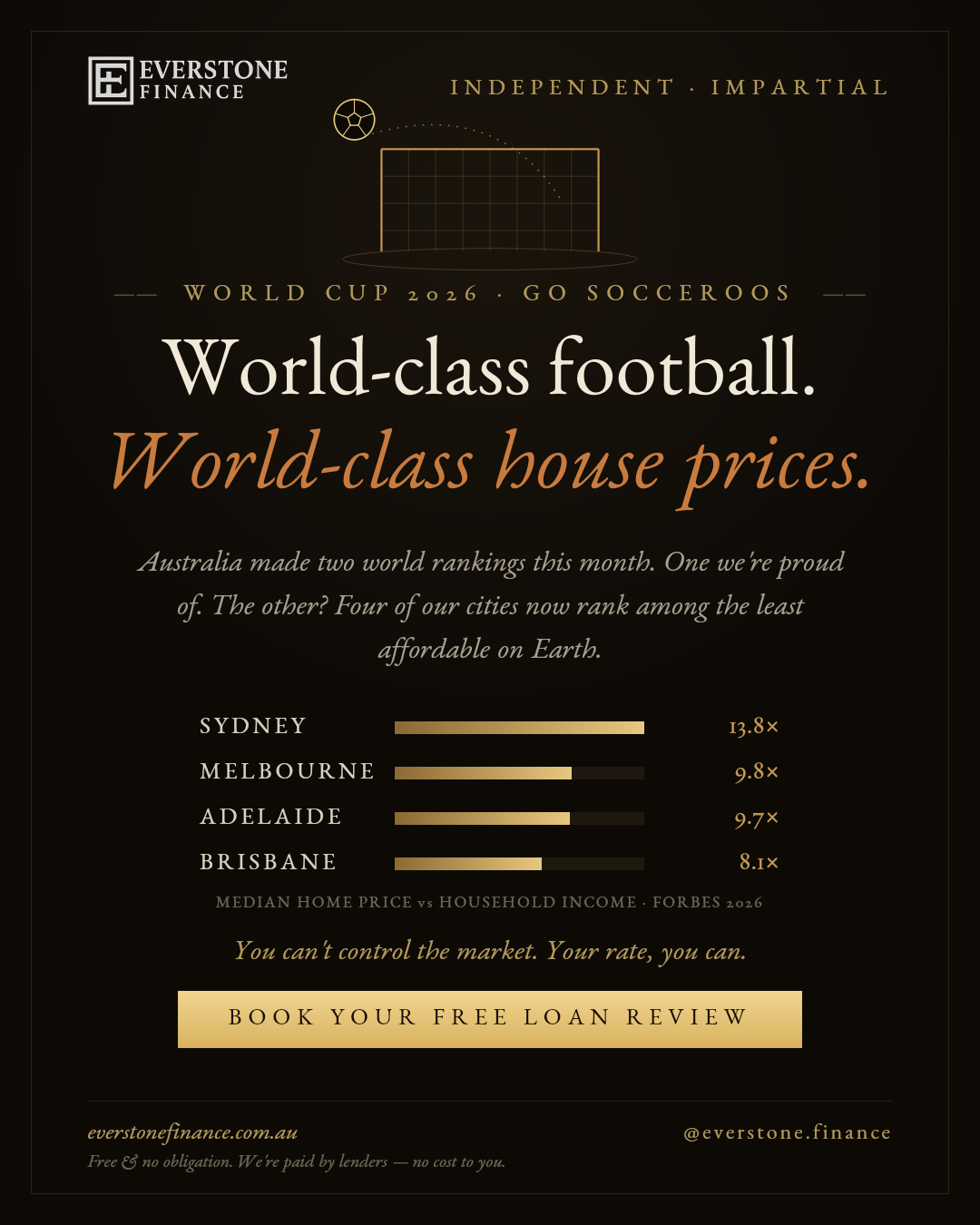

- Four Australian cities rank among the world’s least affordable in Forbes’ 2026 list: Sydney (13.8× income), Melbourne (9.8×), Adelaide (9.7×) and Brisbane (8.1×).

- Sydney is the second least affordable city on Earth, behind only Hong Kong (16.7×). A median Sydney home costs 13.8 years of the median household’s pre-tax income.

- Melbourne is less affordable than San Francisco (9.8× vs 9.4×), and Adelaide is less affordable than San Diego. Brisbane sits level with London.

- No other country places four cities on the list. The United States has six, but with roughly thirteen times Australia’s population.

- You can’t control the market, but you can control your rate. When loans are this large relative to income, even a small rate difference is worth thousands a year, which is why a free loan review matters more in Australia than almost anywhere else.

This week, Australia is on the world stage twice. The Socceroos have kicked off their sixth consecutive FIFA World Cup, opening their Group D campaign against Türkiye, and the whole country is behind them. At Everstone Finance we’re cheering as loudly as anyone. But June 2026 also brought a second world ranking, one nobody celebrates: Forbes’ list of the least affordable cities in the world, measured by median home price against median household income. Four of the cities on it are Australian. This guide breaks down the full ranking, what a price-to-income ratio actually means for your deposit and repayments, why Australian housing got here, and, most importantly, what you can actually do about the one part of the equation you control: your home loan.

The least affordable cities in the world (2026)

The least affordable city in the world in 2026 is Hong Kong, where the median home costs 16.7 times the median household’s pre-tax income (Forbes). Sydney ranks second at 13.8×, ahead of Vancouver (11.8×), San Jose (11.4×) and Los Angeles (10.9×). Melbourne (9.8×), Adelaide (9.7×) and Brisbane (8.1×) also make the list, giving Australia four of the world’s least affordable housing markets.

Forbes measures affordability the way economists do: the median home price for the main dwelling type, divided by median pre-tax household earnings. The result is the number of years a typical household would need to spend its entire gross income to buy the typical home. Here is the full 2026 ranking, with the Australian cities highlighted.

| Rank | City | Country | Price-to-income |

|---|---|---|---|

| 1 | Hong Kong | Hong Kong SAR | 16.7× |

| 2 | Sydney | Australia | 13.8× |

| 3 | Vancouver | Canada | 11.8× |

| 4 | San Jose | United States | 11.4× |

| 5 | Los Angeles | United States | 10.9× |

| 6 | Honolulu | United States | 10.5× |

| 7 | Melbourne | Australia | 9.8× |

| 8 | Adelaide | Australia | 9.7× |

| 9 | San Francisco | United States | 9.4× |

| 10 | San Diego / Toronto | US / Canada | 9.3× |

| 11 | Auckland | New Zealand | 8.2× |

| 12 | Brisbane / London | Australia / UK | 8.1× |

| 13 | Miami | United States | 8.0× |

The headline: Australia is a country of 27 million people with four cities on a global unaffordability list otherwise dominated by the United States (330+ million), Canada and global financial hubs. Per capita, no developed country comes close.

Australia’s four least affordable cities, city by city

Here’s what each Australian entry on the list actually means for the people trying to buy, or already paying off, a home there. Median dwelling values below are from Cotality as at 31 May 2026; for the full capital-city breakdown see our companion guide to median house prices in every Australian capital.

Sydney: 13.8× income, the world’s second least affordable city

Sydney’s median dwelling value of $1,282,020 against median household earnings produces a ratio of 13.8, second only to Hong Kong globally. To put that in football terms: a household saving 10% of its gross income for a 20% deposit needs roughly 27 years of saving before stamp duty. The irony is that Sydney’s prices grew just 2.3% over the past year, among the slowest of the capitals. The unaffordability isn’t momentum, it’s altitude.

Melbourne: 9.8× income, less affordable than San Francisco

Melbourne sits seventh globally at 9.8 times income, ahead of San Francisco (9.4×), one of the world’s most notorious housing markets. That’s despite Melbourne being, by Australian standards, the value story of 2026: its median dwelling value of $812,621 now ranks just sixth among our capitals after a near-flat year. Melbourne’s problem isn’t price growth; it’s that incomes haven’t kept up with two decades of compounding.

Adelaide: 9.7× income, the quiet achiever nobody wanted

Adelaide’s appearance at 9.7× might be the most telling entry on the entire list. Long pitched as the affordable alternative, Adelaide has repriced so fast (up 12.3% over the year to a $950,703 median) that it’s now less affordable relative to local incomes than San Diego or Toronto. When the “cheap” Australian capital out-ranks Californian beach cities for unaffordability, the national pattern is undeniable.

Brisbane: 8.1× income, level with London

Brisbane ties with London at 8.1 times income. After growing 19.1% in a single year to a median of $1,126,149, Brisbane has overtaken Melbourne to become Australia’s second most expensive capital by value, and its income ratio now matches one of the world’s great financial capitals, without the financial-capital salaries. Olympic momentum, interstate migration and tight supply have all done their part.

What does a price-to-income ratio actually mean?

A price-to-income ratio divides the median home price by the median household’s annual pre-tax income. A ratio of 13.8 means the typical home costs 13.8 years of the typical household’s entire gross income. Housing economists generally call a market “severely unaffordable” once the ratio passes 5.1. Every Australian city on the Forbes list is at least 8.

The ratio matters because it translates directly into the two numbers that decide whether you can buy: the deposit and the loan size. The table below shows what each Australian city’s ratio means in years of gross household income, both for a 20% deposit and for the loan itself.

| City | Price-to-income | 20% deposit equals | 80% loan equals |

|---|---|---|---|

| Sydney | 13.8× | 2.8 years of income | 11.0 years of income |

| Melbourne | 9.8× | 2.0 years of income | 7.8 years of income |

| Adelaide | 9.7× | 1.9 years of income | 7.8 years of income |

| Brisbane | 8.1× | 1.6 years of income | 6.5 years of income |

A quick decoder for those columns: a deposit below 20% usually means paying Lenders Mortgage Insurance, though a family guarantor or a profession-based waiver can remove it, and your maximum loan is set by LVR rules. Plain-English definitions for every term live in our mortgage glossary.

Two practical notes. First, a median is a midpoint, not your price: units, townhouses and outer suburbs sit below it, which is why knowing the buying process and your real borrowing power matters more than the headline. Second, these ratios use gross income; after tax, the effective burden is heavier still, which is exactly why the cost of the loan itself deserves so much attention.

How Australia compares with the rest of the world

Australia places four cities on Forbes’ 2026 least-affordable list, more than any other country relative to its size. The United States places six (San Jose, Los Angeles, Honolulu, San Francisco, San Diego, Miami) from a population thirteen times larger. Canada places two (Vancouver, Toronto), and the UK, New Zealand and Hong Kong one each.

The comparison gets starker when you look at what kind of cities surround ours on the list. Hong Kong is one of the densest places on Earth with extreme land scarcity. San Jose and San Francisco sit at the heart of the world’s highest-paying technology industry. London and Toronto are global financial centres. Sydney, Melbourne, Adelaide and Brisbane are spacious, mid-density cities on a vast continent, and they still out-rank most of them. Auckland, our closest cousin in housing-policy terms, sits at 8.2, just above Brisbane.

Why is Australian housing so expensive relative to income?

Three structural forces drive Australia’s housing unaffordability: chronic undersupply (construction has lagged population growth for years), concentrated demand (most Australians live in a handful of capital cities, and record migration flows into the same markets), and two decades of cheap credit capitalised into prices. Interest rates, with the RBA cash rate at 4.35%, now make the resulting loans expensive to carry.

None of this is news to anyone who has tried to buy lately, but the ranking puts a number on it. It also explains the multi-speed market we covered in our capital-city median price guide: the cheaper capitals (Perth, Brisbane, Adelaide, Darwin) have been growing at double-digit rates as buyers chase relative affordability, which in turn erodes the very affordability they were chasing. Adelaide’s arrival on a global unaffordability list is that loop completing itself.

For what higher rates specifically do to your borrowing power, our companion piece on interest rates and the 4.35% cash rate walks through the numbers.

What unaffordability actually costs you, every month

Here’s the part of the story that doesn’t make headlines. A high price-to-income ratio doesn’t just make homes hard to buy, it makes the loans behind them enormous relative to the incomes servicing them. And when the loan is enormous, the interest rate on it matters more than almost anywhere else in the world.

- On a $600,000 loan, a difference of 0.50 percentage points in your rate is roughly $3,000 a year in interest, every year.

- On an $800,000 loan, the same gap is roughly $4,000 a year.

- On a $1,000,000 Sydney-sized loan, it’s roughly $5,000 a year, the price of a family holiday, lost to a rate you never renegotiated.

This is also where the loyalty tax bites. Lenders compete hardest for new customers, while existing borrowers drift onto higher rates year after year. In a low-priced market, that drift is an annoyance. In a market where the median home costs 8 to 14 times income, it compounds into serious money. The RBA and ACCC have both documented the gap between rates paid by new and existing borrowers; in a country this unaffordable, leaving it unchecked is the single most expensive financial habit a household can have.

You can’t control the market. You can control your rate.

You can’t change Australia’s housing supply, migration settings or the RBA cash rate. You can change the rate you pay on your own loan. Reviewing your home loan, with a broker comparing 30+ lenders, is free, takes less time than a football match, and is the one lever every borrower in an unaffordable market fully controls.

The Socceroos can’t control the draw, the referee or the weather in Vancouver. What they control is preparation, and that’s the whole game plan. The same logic applies to your mortgage. The market handed Australian borrowers some of the largest loans, relative to income, on the planet. The only question that remains within your control is whether that loan is priced as sharply as the market allows today, not whenever you last signed.

When we review a loan at Everstone, we’re ex-bankers comparing your current rate, structure and features against 30+ lenders. Sometimes the answer is “your loan is still competitive, keep it”, and we’ll tell you that plainly. Often it isn’t, and the difference funds something that matters more to you than your bank’s margin.

How to make your home loan match fit: a 5-point checklist

To get your loan match fit: 1) find your current interest rate (most borrowers can’t name it), 2) check when your fixed term expires and what revert rate follows, 3) confirm your loan has the features you actually use (offset, redraw), 4) compare against the wider market, not just your own bank’s “retention” offer, and 5) weigh switching costs against savings, a broker does steps 4 and 5 for you at no cost.

1. Know your number

Pull up your statement or app and find your actual rate. If you haven’t looked in over two years, the odds you’re on a market-leading rate are slim.

2. Check your fixed-rate expiry

Loans rolling off fixed terms often land on a revert rate well above what a new customer would be offered. Diarise the expiry and start the review three months out.

3. Audit your features

An offset account you actually use can save more than a slightly lower headline rate; one you pay an annual fee for and never use does the opposite. Structure should match how you live.

4. Compare the whole field

Ringing your own bank for a discount is a half-measure: they only need to beat your inertia, not the market. A broker compares 30+ lenders and negotiates with your full position in hand. Not sure how to choose one? Here are the questions to ask a mortgage broker before you commit.

5. Count the costs honestly

Discharge fees, government fees and any new-loan costs typically total a few hundred to around a thousand dollars. Against savings of thousands per year on loans this size, the maths usually resolves quickly, but it should always be done in writing before you move.

Get your loan match fit, free

Book a no-obligation review and we’ll compare your current loan against 30+ lenders, in less time than a World Cup match, and show you the result in plain English.

Book an appointmentSources and useful references

Housing affordability glossary

- Price-to-income ratio

- The median home price divided by median annual pre-tax household income. The standard international measure of housing affordability; higher means less affordable.

- Median multiple

- Another name for the price-to-income ratio. Markets above 5.1 are conventionally classed as “severely unaffordable” by housing researchers.

- Median household income

- The midpoint of all household incomes in a market, measured pre-tax in the Forbes data. Half of households earn more, half earn less.

- Loyalty tax

- The gap between the interest rates lenders offer new customers and the higher rates existing borrowers drift onto over time. Avoided by regularly reviewing or refinancing your loan.

- Refinancing

- Replacing your current home loan with a new one, with your existing lender or a new one, to get a better rate, structure or features. Usually free to explore through a broker.

- Revert rate

- The variable rate your loan automatically rolls onto when a fixed term ends. Often significantly higher than rates offered to new borrowers.

- Offset account

- A transaction account linked to your loan whose balance reduces the loan amount on which interest is charged. On large Australian loan sizes, a well-used offset is powerful.

- Borrowing power

- The maximum a lender will lend you based on income, expenses, debts and their assessment rate. It varies between lenders, which is why comparing the whole market matters.

Least affordable cities FAQ

What are the least affordable cities in the world in 2026?

According to Forbes’ 2026 ranking by median home price-to-income ratio: Hong Kong (16.7×), Sydney (13.8×), Vancouver (11.8×), San Jose (11.4×), Los Angeles (10.9×), Honolulu (10.5×), Melbourne (9.8×), Adelaide (9.7×), San Francisco (9.4×), San Diego and Toronto (9.3×), Auckland (8.2×), Brisbane and London (8.1×), and Miami (8.0×).

How many Australian cities are among the world’s least affordable?

Four: Sydney (13.8× income), Melbourne (9.8×), Adelaide (9.7×) and Brisbane (8.1×). No other country places as many cities on the list relative to its population.

Is Sydney the least affordable city in the world?

Sydney is the second least affordable city in the world in 2026, behind only Hong Kong. The median Sydney home costs 13.8 times the median household’s annual pre-tax income.

Is Melbourne really less affordable than San Francisco?

Relative to local incomes, yes. Melbourne’s price-to-income ratio of 9.8 exceeds San Francisco’s 9.4 in the 2026 Forbes data. San Francisco’s homes cost more in absolute dollars, but its household incomes are far higher.

What is a house price-to-income ratio?

It divides the median home price by the median household’s annual pre-tax income, giving the number of years of gross income the typical home costs. Researchers class anything above 5.1 as severely unaffordable; every Australian city on the list is 8 or above.

Why are Australian house prices so high compared to incomes?

The main structural drivers are chronic housing undersupply, population and migration concentrated into a handful of capital cities, and two decades of falling interest rates capitalised into prices. With the cash rate now at 4.35%, the resulting large loans are also expensive to carry.

What does housing unaffordability mean for my home loan?

It means your loan is large relative to your income, so every fraction of a percent on your rate is worth more. On an $800,000 loan, a 0.50 percentage point rate difference is roughly $4,000 a year, which is why regular loan reviews matter more in Australia than in most countries.

How can I lower my mortgage repayments in an expensive market?

The main levers are negotiating or refinancing to a sharper rate, using an offset account effectively, restructuring your loan term or repayment type to suit your situation, and removing features you pay for but don’t use. A broker can model all of these for you at no cost.

When should I review or refinance my home loan?

Good triggers: it’s been more than two years since your last review, your fixed rate is expiring within three months, your property value has risen materially, or your loan lacks features you now need. If any of those apply, a review is worth the half hour.

Does a home loan review cost anything with a broker?

No. Brokers like Everstone Finance are paid by the lender when a loan settles, so reviews and comparisons are free to you, with no obligation to act on the findings.

Where does this affordability data come from?

The price-to-income ratios are from Forbes’ 2026 ranking of the least affordable cities, where price reflects the main dwelling type and income is median pre-tax household earnings. Australian median dwelling values referenced are from Cotality as at 31 May 2026. Figures change over time; confirm the latest before acting.

Do I need to be in Melbourne or South Yarra to work with Everstone Finance?

No. Everstone Finance is based in South Yarra and meets locally in person, but works with clients across Melbourne and Australia-wide by phone and Zoom.

The bottom line: Australia is world class at football this month, and world class at housing unaffordability all year round, with four cities on the 2026 global list. You can’t control the market, migration or the cash rate. You can control the rate on your own loan, and on Australian-sized loans, that single controllable number is worth thousands a year. Back the Socceroos, and back yourself.

Review your loan in less time than a match

No cost, no obligation. We’ll compare your rate, structure and features against 30+ lenders and tell you honestly whether to move or stay, clearly and in writing.

Book an appointment