90% LMI Waiver for Professionals (2026): Borrow to 90% With No LMI for Doctors, Lawyers, Accountants, Bankers, Tech & Government

Eligible professionals can borrow to 90% LVR with Lenders Mortgage Insurance waived (select lenders, 2026).

- Select lenders waive Lenders Mortgage Insurance for eligible professionals, letting you borrow up to 90% of a property’s value with no LMI, a 10% deposit instead of the usual 20%, without the insurance bill.

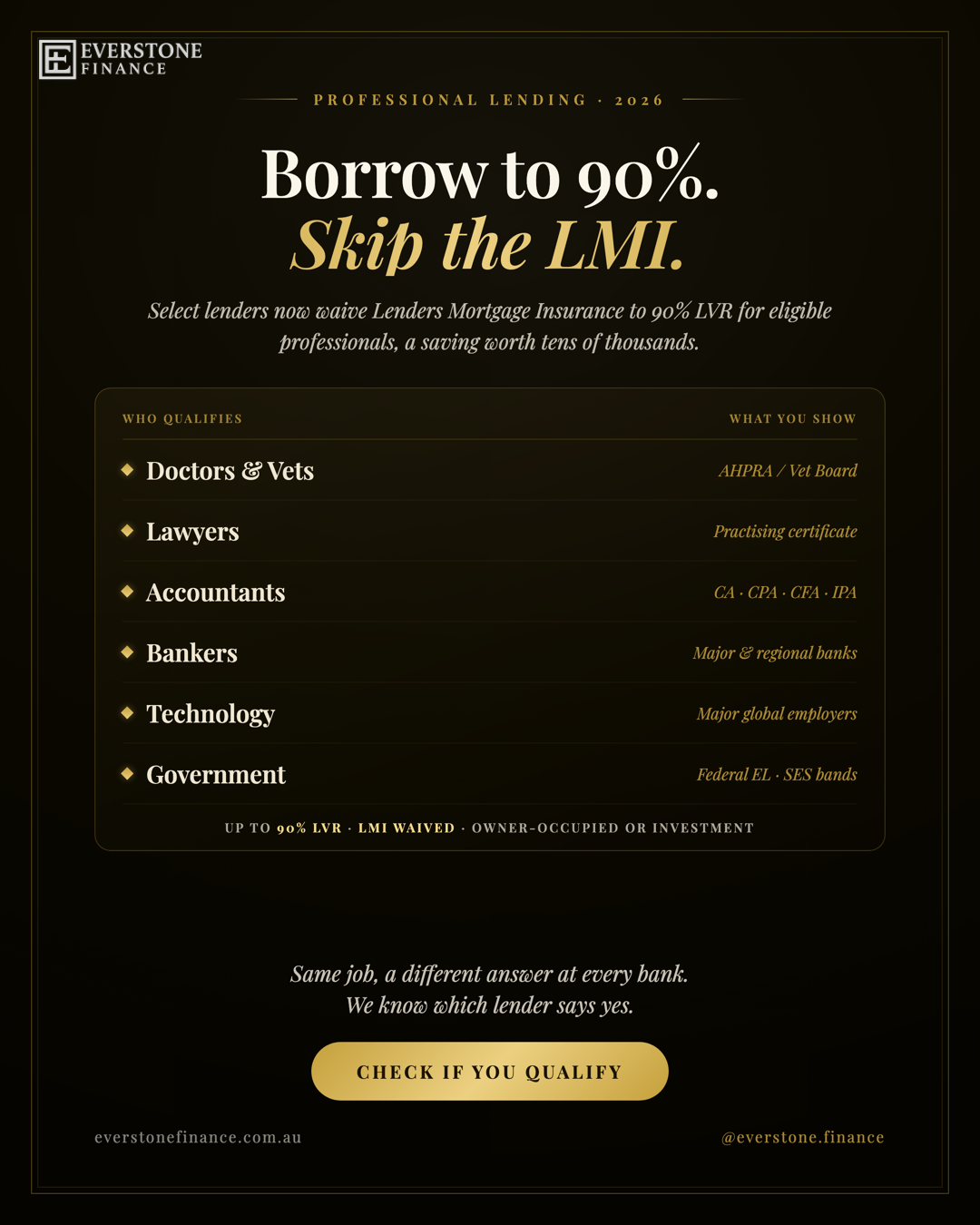

- It now spans far more than doctors. Eligible groups include medical and health practitioners, veterinarians, lawyers, accountants, banking and finance employees, technology-sector employees and senior federal government staff.

- The saving runs into the tens of thousands. On a typical metro purchase, the LMI you avoid is often $15,000 to $30,000+, money that stays in your pocket or boosts your deposit.

- It works for more than first homes. Depending on the lender, the waiver can apply to owner-occupied or investment purchases, and to refinances, loans up to around $5 million.

- The catch is the panel, not the policy. Eligibility lists, employers and limits differ sharply between lenders and change without notice. The same job can be approved at one lender and declined at the next, which is exactly what a broker is for.

For years, the “no LMI” conversation in Australian lending was a doctors-only club. That has changed. As of June 2026, the professional Lenders Mortgage Insurance waiver has widened well beyond medicine, lawyers, accountants, bankers, technology employees, vets and senior public servants can now, at select lenders, borrow to 90% of a property’s value with the LMI premium waived entirely. At Everstone Finance we are ex-bankers who wrote and assessed these policies from the inside; this guide explains what the waiver is, what it’s worth, exactly which professions qualify, and the one thing that trips people up, the fact that it is never a single, universal policy.

What is the professional LMI waiver?

A professional LMI waiver lets borrowers in eligible occupations take out a home loan up to 90% of the property’s value (90% LVR) without paying Lenders Mortgage Insurance. Normally, any loan above 80% LVR triggers LMI, a one-off premium that protects the lender, not you, and can cost many thousands of dollars. The waiver removes it, so a 10% deposit behaves like a 20% one on cost, without the insurance.

Lenders offer this because eligible professionals are, statistically, lower-risk borrowers: stable, high earning, with secure career trajectories. Removing LMI is how lenders compete for them. The mechanics are simple, but the details matter:

- Up to 90% LVR, LMI waived, a 10% deposit, no insurance premium. (Doctors and some medical specialists can often go further still, up to 95% LVR with no LMI, under a separate, stronger tier; see our home loans for doctors guide.)

- Owner-occupied or investment, purchase or refinance, depending on the lender, the waiver isn’t limited to first homes.

- Large loan sizes, commonly up to around $5 million, which puts genuine metropolitan purchases comfortably within reach.

- Evidence-based, you prove your profession with registration, a practising certificate, professional membership or employer confirmation (set out by category below).

If the terms LMI and LVR are new to you, our plain-English explainers on what LMI is and what LVR means cover the fundamentals, and every term is defined in our mortgage glossary.

What the waiver actually saves you

LMI on a 90% lend is typically 1.5% to 2.5% of the loan amount, so on most metropolitan purchases the waiver saves somewhere between $15,000 and $35,000+. The exact premium depends on the loan size, the LVR, the insurer and whether you’re a first-home buyer, but it is always a four- or five-figure saving you keep.

The table below shows indicative LMI premiums that an eligible professional would avoid at 90% LVR. Treat these as illustrative ranges only, actual LMI varies by lender, insurer and circumstances, but they show the order of magnitude.

| Purchase price | 10% deposit | Loan (90% LVR) | Indicative LMI avoided |

|---|---|---|---|

| $700,000 | $70,000 | $630,000 | ~$11,000 to $18,000 |

| $900,000 | $90,000 | $810,000 | ~$15,000 to $24,000 |

| $1,200,000 | $120,000 | $1,080,000 | ~$22,000 to $33,000 |

| $1,500,000 | $150,000 | $1,350,000 | ~$28,000 to $45,000 |

Two ways to use the saving: keep it, the LMI you don’t pay stays in your offset working against your interest, or redeploy it, putting it toward a slightly larger purchase or your costs (stamp duty, legals). Either way, it’s a five-figure head start over an identical borrower in a different job.

Who qualifies? The eligible professions, one by one

The waiver now covers a broad set of occupations. Below is who typically qualifies and the evidence usually required. Eligibility, employer lists and limits vary between lenders and change over time, so treat this as a map, not a guarantee, we confirm your exact position against current lender policy before you apply.

Medical & health practitioners

Registered medical practitioners and a wide range of health professionals, from GPs and specialists to many allied-health roles, are the original and strongest category. Many doctors access an even higher tier (up to 95% LVR, no LMI). Evidence: current AHPRA registration. See our dedicated doctors’ home loan guide for the medical-specific tiers.

Veterinarians

Registered vets qualify under the professional waiver in their own right. Evidence: current registration with the relevant state or territory veterinary board.

Lawyers

Admitted legal practitioners, solicitors, barristers and partners, who hold a current practising certificate in Australia. Evidence: a current Australian practising certificate. Our home loans for lawyers guide covers the legal profession in full.

Accountants

Qualified accountants who are members of a recognised professional body, including Chartered Accountants ANZ, CPA Australia, the CFA Institute or the Institute of Public Accountants. Evidence: current professional membership. Our accountants’ lending guide goes deeper, including the EOFY angle.

Banking & finance employees

PAYG employees of Australia’s major and second-tier banks can qualify, usually with a minimum period of continuous employment. This is a newer addition that recognises stable, salaried finance-sector income. Evidence: employment contract or letter, or a recent payslip confirming your employer and tenure.

Technology-sector employees

Directly employed (not agency-contracted) PAYG staff at major global technology employers can qualify, typically after a minimum period of continuous employment. Evidence: an employment contract or letter on company letterhead, or a payslip stating your start date.

Federal government employees

Ongoing employees of federal government departments at senior classifications, broadly the Executive Level (EL) and Senior Executive Service (SES) bands, can qualify, where directly employed. Evidence: an employment contract or letter and/or current payslip confirming your employer and band.

Not on this list? The professional categories keep widening, and the higher-LVR medico tier, guarantor options and the government’s low-deposit schemes can achieve a similar result for buyers outside these occupations. The honest answer to “do I qualify?” is almost always “let’s check against current policy”, it takes minutes.

Going deeper by profession: this guide is the cross-profession overview. For the full detail on your occupation, including the higher 95% medico tier and the profession-specific quirks, see our dedicated guides for doctors, accountants, lawyers, nurses and teachers.

How the waiver stacks with everything else

The LMI waiver isn’t an either/or. For eligible borrowers it generally combines with the rest of a competitive loan:

- Professional package discounts, many lenders pair waivers with sharper rates and fee waivers for the same professional borrowers.

- Not first-home-only, depending on the lender, it applies to upgraders, refinancers and (often) investors, not just first purchases.

- Offset and structure, the deposit you save on LMI can sit in an offset account, reducing your interest from day one.

If you’re a first-home buyer, it’s worth comparing the waiver against the federal Home Guarantee Scheme and state grants: under the price caps, a government guarantee can be simpler; above them, the professional waiver is often the only low-deposit path that avoids LMI. The right choice depends on your price point and goals.

The catch: it’s never just one policy

There is no single, industry-wide professional LMI waiver. Each lender runs its own version, with its own eligible-occupation list, employer list, minimum-tenure rules, maximum LVR and loan caps, and they change without notice. The same borrower, in the same job, can be approved at one lender and declined at another. Choosing the right lender, in the right order, is the whole game.

This is where the policy looks deceptively simple and is anything but. One lender’s accountant list might require a specific body; another’s tech list might include your employer when a competitor’s doesn’t; a third might cap investment lending lower than owner-occupied. We spent a decade inside the banks writing exactly these rules. Now we sit on the other side and match the professional to the lender, rather than hoping the one bank you happened to walk into says yes.

Why use Everstone for a professional-waiver loan

A single bank can only check you against its own list. If your profession or employer isn’t on it, you simply hear “no”, and you rarely learn that the lender across the road would have said yes. As independent brokers comparing 30+ lenders, we know which panels currently recognise your occupation and employer, where the LVR and loan caps sit, and how to package your application so the waiver actually lands.

We’re paid by the lender when your loan settles, so checking your eligibility and comparing the market is free to you, and under the Best Interests Duty we’re legally bound to work in your interest. If you’re weighing your options, here are the questions worth asking a broker first.

Find out if your profession waives the LMI

Tell us your occupation and employer, and we’ll check it against current lender policy across 30+ lenders, and show you what borrowing to 90% with no LMI looks like for your purchase. No cost, no obligation.

Check if you qualifySources and useful references

Professional lending glossary

- Lenders Mortgage Insurance (LMI)

- A one-off insurance premium that protects the lender (not you) when you borrow more than 80% of a property’s value. It can cost many thousands of dollars and is exactly what a professional waiver removes.

- Loan-to-value ratio (LVR)

- The loan as a percentage of the property’s value. A 10% deposit is a 90% LVR. Loans above 80% LVR normally attract LMI unless a waiver applies.

- Professional LMI waiver

- A lender policy that removes LMI for borrowers in eligible occupations, typically up to 90% LVR (and up to 95% for some medical roles), recognising them as lower-risk borrowers.

- Professional package

- A bundled home-loan product offering rate and fee discounts for qualifying professionals, often paired with the LMI waiver.

- Genuine savings

- Funds you have accumulated or held over time (rather than a sudden gift or windfall), which some lenders require for higher-LVR lending. Policy varies by lender.

- Owner-occupied vs investment

- Whether you’ll live in the property or rent it out. Some waivers apply to both; caps and conditions can differ between the two.

Professional LMI waiver FAQ

What is the 90% LMI waiver for professionals?

It is a lender policy that lets eligible professionals borrow up to 90% of a property’s value without paying Lenders Mortgage Insurance. Instead of needing a 20% deposit to avoid LMI, a qualifying professional can put down 10% and still skip the premium. Some medical roles can go to 95% LVR with no LMI under a stronger tier.

Which professions qualify for an LMI waiver in 2026?

Depending on the lender, eligible groups include registered medical and health practitioners, veterinarians, lawyers (with a current practising certificate), accountants (members of a recognised body such as CA ANZ, CPA, CFA or IPA), employees of major and second-tier banks, technology-sector employees at major global employers, and senior federal government staff (EL and SES bands).

How much can the LMI waiver save me?

LMI on a 90% loan is typically 1.5% to 2.5% of the loan amount, so the waiver commonly saves between $15,000 and $35,000 or more on a metropolitan purchase. The exact figure depends on the loan size, LVR, insurer and your circumstances. These are estimates, not quotes.

Do I still need a deposit with the LMI waiver?

Yes. The waiver removes the insurance premium, not the deposit. You generally still need a 10% deposit (a 90% LVR loan), plus funds for purchase costs such as stamp duty and legals. The benefit is avoiding LMI on top of that.

Does the LMI waiver apply to investment properties?

At some lenders, yes, the waiver can apply to owner-occupied or investment purchases, and to refinances, though caps and conditions can differ. It is not limited to first-home buyers at most lenders. Always confirm the specific lender’s policy.

I’m a doctor, is this the same as the doctor home loan?

It’s related but stronger for you. Many lenders offer doctors and certain medical specialists an even higher tier, up to 95% LVR with no LMI, on top of the 90% professional waiver others receive. Our home loans for doctors guide covers the medical-specific tiers in detail.

How do I prove my profession qualifies?

It depends on the category: AHPRA registration for medical practitioners, state board registration for vets, a current practising certificate for lawyers, professional-body membership for accountants, and an employment contract, letter or payslip for banking, technology and government employees. Your broker confirms exactly what each lender needs.

Why would one lender approve my profession and another decline it?

Because there is no single industry policy. Each lender maintains its own list of eligible occupations and employers, its own minimum-tenure rules and its own LVR and loan caps, and these change without notice. Matching your profession and employer to a lender that currently recognises them is why working with a broker matters here.

Is the LMI waiver available for large loans?

Yes, eligible professionals can often access the waiver on loans up to around $5 million, depending on the lender, which covers most metropolitan purchases. Higher loan sizes and LVRs can affect conditions, so the specifics are confirmed case by case.

Does checking my eligibility with Everstone cost anything?

No. Everstone Finance is paid by the lender when a loan settles, so checking which lenders recognise your profession and comparing the market is free to you, with no obligation to proceed.

Do I need to be in Melbourne to work with Everstone Finance?

No. Everstone Finance is based in South Yarra and meets locally in person, but works with professional clients across Melbourne and Australia-wide by phone and Zoom.

The bottom line: If you’re a doctor, vet, lawyer, accountant, banker, tech employee or senior public servant, your profession may let you borrow to 90% with no LMI, a five-figure saving and a smaller deposit. The waiver is real and widening; the trap is assuming it works the same everywhere. It doesn’t. Get the lender match right, and the policy pays you.

Borrow to 90% with no LMI

We’ll check your profession and employer against current policy across 30+ lenders and show you exactly what it means for your deposit and your purchase, in plain English, in writing.

Check if you qualify