Where Investors Get the Best Return in 2026: Rental Yields vs the Cost to Hold, Every Australian Capital

Gross rental yield against the cost to hold, across Australia’s capital cities (Cotality, May 2026).

- Darwin leads every Australian capital on gross rental yield at 6.0%, and it’s also the cheapest to hold, roughly $2,660 a month interest-only on the median dwelling (Cotality, May 2026).

- Sydney has the lowest yield (3.1%) and the highest cost, around $5,380 a month interest-only. Brisbane (3.3%), Adelaide (3.4%) and Perth (3.6%) sit in between.

- High yield and high growth rarely live in the same city. The capitals with the strongest yields are usually the ones with the thinner long-run growth story, so “best return” depends entirely on your strategy.

- Gross yield ignores the costs that decide your actual return: rates, insurance, management, maintenance, vacancy, and, above all, the interest rate and structure of your loan.

- The one lever you fully control is the financing. On a $700,000 investment loan, a 0.40% rate difference is about $2,800 a year, which is why investors compare 30+ lenders, not one.

A chart did the rounds on LinkedIn this month asking a deceptively simple question: if you were buying purely on today’s numbers, which city would you choose? It ranked every Australian capital by gross rental yield against the monthly cost of holding the median dwelling. At Everstone Finance we look at versions of that question every week with investor clients, so this guide takes the data further: what the yields actually mean, why the highest-yielding city isn’t automatically the best investment, and the part of the equation most investors underweight, how the loan behind the property is priced and structured. Because that last part is the only number on the page you fully control.

Rental yields and the cost to hold, every Australian capital (2026)

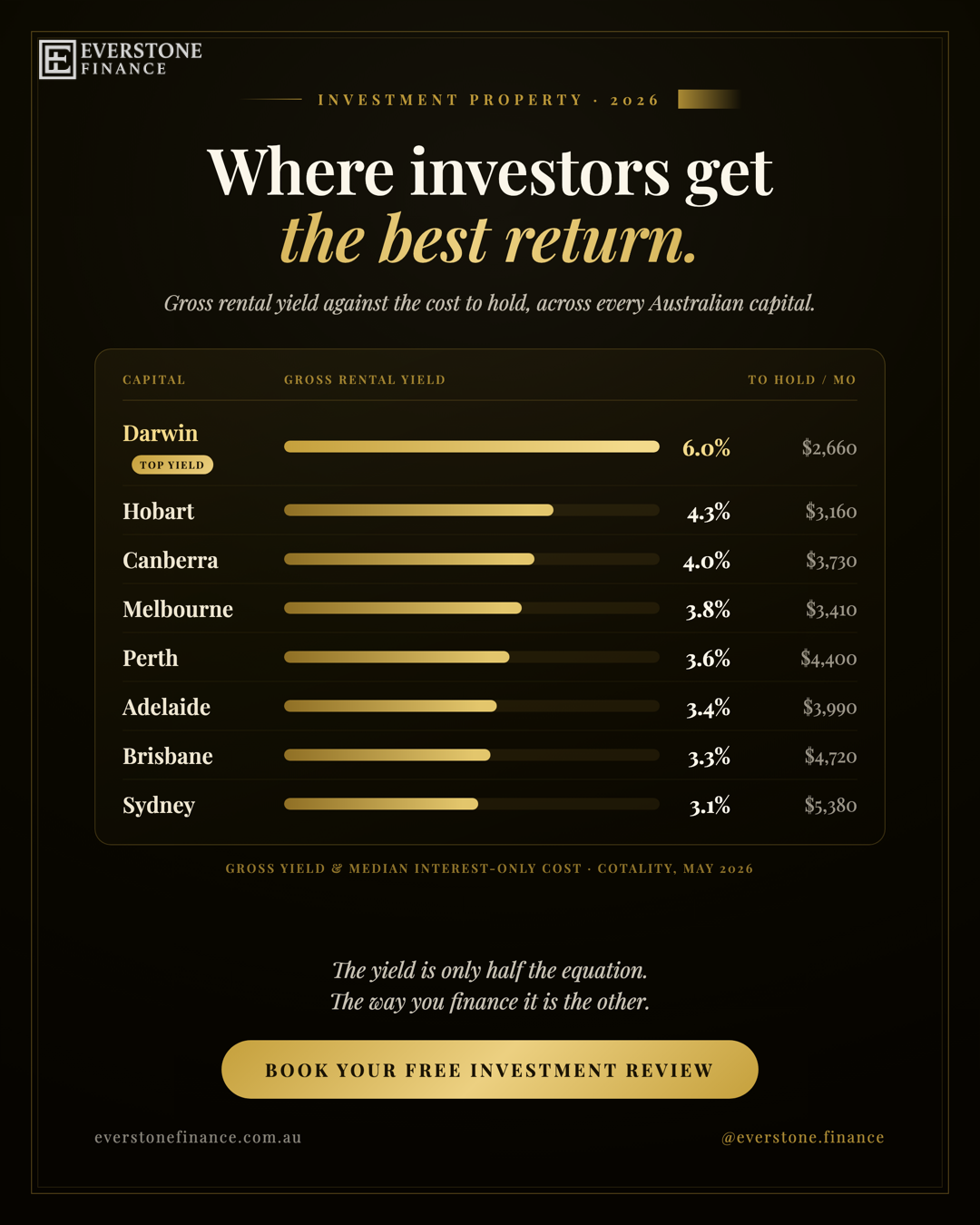

On 2026 figures, Darwin offers the highest gross rental yield of any Australian capital at 6.0%, followed by Hobart (4.3%), Canberra (4.0%) and Melbourne (3.8%). Sydney is the lowest at 3.1%, with Brisbane (3.3%), Adelaide (3.4%) and Perth (3.6%) in between. The higher-yielding capitals are also, broadly, the cheaper ones to buy and hold.

The table below ranks every capital by gross rental yield, alongside the median dwelling value and the indicative monthly cost to hold it interest-only. The cost column assumes a 20% deposit (an 80% loan) at an interest-only rate of 6.29% p.a. on the median value, the same basis as the widely shared source chart.

| Rank | City | Gross yield | Median value | Monthly cost (IO) |

|---|---|---|---|---|

| 1 | Darwin | 6.0% | $634,000 | $2,660 |

| 2 | Hobart | 4.3% | $754,000 | $3,160 |

| 3 | Canberra | 4.0% | $890,000 | $3,730 |

| 4 | Melbourne | 3.8% | $813,000 | $3,410 |

| 5 | Perth | 3.6% | $1,049,000 | $4,400 |

| 6 | Adelaide | 3.4% | $952,000 | $3,990 |

| 7 | Brisbane | 3.3% | $1,126,000 | $4,720 |

| 8 | Sydney | 3.1% | $1,283,000 | $5,380 |

Read it this way: Darwin’s investor pays the least each month and collects the most rent per dollar invested. Sydney’s investor pays the most and collects the least, because in Sydney you are paying for expected capital growth, not income. Neither is “better”; they’re different jobs for your money.

So which city gives investors the best return?

There is no single best city, it depends on whether you’re investing for income (yield) or capital growth. On pure income today, Darwin (6.0%) leads. For long-run growth, investors have historically favoured the larger east-coast capitals despite their lower yields. The right answer is the city whose strengths match your strategy, your borrowing capacity and your tax position, not simply the biggest number in a column.

The chart that prompted this guide is a great conversation starter and a poor decision-maker, because it measures one thing (gross yield) and stops. A property’s total return is yield plus capital growth, minus holding costs, minus the cost of the money you borrowed to buy it. Darwin wins decisively on the first term and the last; it has historically been far more volatile on the second. Sydney is the mirror image. Most of the country sits somewhere between.

Yield versus growth: the trade-off every investor has to price

Australian property pays you in two currencies. Rental yield is the income the tenant pays, expressed as a percentage of the property’s value. Capital growth is the change in the property’s value over time. The two tend to pull in opposite directions across the capitals, and understanding why is most of the game.

High-yield markets: income now, growth uncertain

Darwin’s 6.0% yield is real, and on a sub-$650,000 entry price the rent can come close to covering the interest from day one. The trade-off is that Darwin’s economy leans heavily on resources and defence, its population is small, and its price history has been the most cyclical of the capitals. You are buying strong cashflow and accepting a less certain growth path. Regional high-yield markets and many apartments tell a similar story.

Low-yield markets: you’re paying for growth

Sydney’s 3.1% yield looks unappealing in isolation, but income was never the point. Investors accept a low yield (and the resulting cashflow gap) because they expect the asset to appreciate, and because deep, diversified city economies tend to support that over decades. The risk is the opposite of Darwin’s: you carry a larger shortfall every month, so your serviceability and your loan structure have to be bulletproof. For the bigger picture on why these cities cost what they do, see our guide to Australia’s place on the global affordability ranking and our median house prices in every capital.

The middle: Melbourne, Brisbane, Adelaide, Perth

Melbourne (3.8%) is the value story among the big capitals after a near-flat few years; Perth, Adelaide and Brisbane have re-rated hard chasing relative affordability, lifting prices and compressing yields in the process. These are the markets where the financing decision, rate, structure and which lender, most often tips a deal from marginal to worthwhile.

What “gross yield” quietly leaves out

Gross yield is annual rent divided by property value, before any costs. Net yield subtracts the real costs of ownership, council rates, insurance, property management, maintenance, strata (if applicable) and vacancy. Net yield is typically 1 to 2 percentage points below gross, which is why a 3.1% gross yield can mean very thin or negative cashflow once the mortgage is added.

Every yield figure in the table above is gross. Before you bank any of it, a real portfolio pays:

- Council rates and water, fixed, unavoidable, and rising.

- Landlord insurance and building insurance, more again for apartments via strata levies.

- Property management, typically 5 to 8% of rent if you don’t self-manage.

- Maintenance and repairs, budget a buffer; older or coastal stock costs more.

- Vacancy, even a fortnight a year is real money against the yield.

None of those costs appears on a yield chart, and all of them are dwarfed by the single largest line item in any geared investment: the interest on the loan.

The cashflow reality: rent against the mortgage

Put the rent and the interest side by side and the strategy choice becomes concrete. Using the table’s own assumptions (median value, 80% loan, interest-only at 6.29%), the implied gross rent against the monthly interest looks like this at the two extremes:

| City | Gross yield | Implied gross rent / mo | Interest-only / mo | Gross gap / mo |

|---|---|---|---|---|

| Darwin | 6.0% | ~$3,170 | $2,660 | +$510 |

| Melbourne | 3.8% | ~$2,575 | $3,410 | −$835 |

| Sydney | 3.1% | ~$3,315 | $5,380 | −$2,065 |

Even before a single holding cost, Darwin’s rent broadly covers its interest, while a Sydney investor funds a two-thousand-dollar-a-month gap out of their own pocket in exchange for expected growth. That gap is what the tax system’s negative gearing rules are designed around, and it’s also exactly what your lender stress-tests when deciding how much you can borrow. Get the structure wrong and the gap quietly caps the size of your next purchase.

The number you actually control: how the loan is priced and structured

You can’t move a city’s yield or its growth outlook. You can control the interest rate, repayment type, structure and lender behind your investment loan, and on investment-sized debt, those decisions are worth thousands a year and can change how many properties you’re able to buy at all. This is the part a broker comparing 30+ lenders is built to optimise.

Two investors can buy the identical apartment in the identical street and end up with very different returns, purely on the financing. Here’s where the difference is made:

The interest rate

Investment rates sit above owner-occupier rates, and the spread between lenders is wide. On a $700,000 investment loan, a 0.40% difference is roughly $2,800 a year, every year, straight off your net yield. Over a typical hold, that compounds into serious money.

Interest-only versus principal and interest

Interest-only keeps monthly outgoings down and is common for investors (it’s the basis of the table above), but it isn’t free: rates are usually higher, the term is limited, and the principal still has to be repaid. P&I builds equity faster. The right answer depends on your cashflow, your tax position and your plans for the property, it’s a structure decision, not a default.

Borrowing capacity differs by lender

This is the one most investors never see. Lenders assess rental income differently (many “shade” it to 75 to 80%), treat existing debts and living costs differently, and apply different assessment buffers. The same investor can be told they can borrow $700,000 at one lender and $900,000 at another. For a portfolio builder, choosing the lender that reads your position most favourably, in the right order, is the difference between buying the next property and being told no.

Structure for the long game

Offset accounts, splitting loans, keeping investment and owner-occupier debt cleanly separated for tax, and releasing equity to fund the next deposit, these are structural choices that either set up your next purchase or quietly block it. They’re decided when the loan is written, not afterwards.

Why property investors work with a broker, not a branch

A bank can only offer you its own product, assessed on its own rules. When that single lender shades your rent hard or caps your borrowing, the deal simply doesn’t happen, and you rarely find out what a different lender would have said. At Everstone, we’re ex-bankers who now compare 30+ lenders on your behalf: matching your income, rental position and goals to the lender most likely to say yes, on the sharpest rate and the structure that supports your next move.

We’re paid by the lender when a loan settles, so the review and the comparison are free to you, and under the Best Interests Duty we’re legally obliged to work in your interest, not a bank’s. If you’re weighing your first investment or your fifth, here are the questions worth asking a broker before you commit.

A worked example: same property, two financing outcomes

Take a $750,000 investment purchase with a 20% deposit, so a $600,000 loan. Consider two scenarios that are entirely within the financing, not the property:

- Rate: a 0.45% difference on $600,000 is about $2,700 a year. Over a five-year hold, roughly $13,500, before compounding.

- Capacity: if the lender that shades your rent least lets you borrow enough to add a second property two years sooner, the value isn’t a rate saving, it’s an extra growing asset on your balance sheet.

The property delivered the yield and the growth. The financing decided how much of it you kept, and whether you could do it again. This is illustrative only, your actual rate, capacity and outcome depend on your circumstances and the lender, but the shape of it is what we model for investors every week.

Buying an investment property? Get the financing right first

Before you choose a city, find out what you can actually borrow, at what rate, and how to structure it for the next purchase. We’ll compare 30+ lenders and show you the numbers in plain English, no cost, no obligation.

Book an appointmentSources and useful references

Property investment glossary

- Gross rental yield

- Annual rent divided by the property’s value, expressed as a percentage, before any ownership costs. The headline figure on most yield charts.

- Net rental yield

- Gross yield after deducting the real costs of ownership (rates, insurance, management, maintenance, strata, vacancy). Typically 1 to 2 percentage points below gross.

- Capital growth

- The increase in a property’s value over time. Together with rental income, it makes up an investment’s total return.

- Positive vs negative gearing

- A property is positively geared when rent exceeds costs (income now), and negatively geared when costs exceed rent (a shortfall you fund, usually betting on growth and tax benefits).

- Interest-only (IO)

- A repayment type where you pay only interest for a set period, keeping monthly outgoings lower but not reducing the loan balance. Common for investors; usually carries a higher rate.

- Rental shading

- The practice of lenders counting only part of your rental income (often 75 to 80%) when assessing serviceability, to allow for costs and vacancy. The shading rate differs by lender.

- Borrowing capacity (serviceability)

- The maximum a lender will lend based on income, expenses, existing debts and an assessment buffer. It varies significantly between lenders for the same borrower.

- Loan-to-value ratio (LVR)

- The loan amount as a percentage of the property’s value. A 20% deposit means an 80% LVR. Higher LVRs may attract Lenders Mortgage Insurance.

- Rentvesting

- Renting where you want to live while owning an investment property where the numbers work better. A common way to enter the market in high-priced cities.

Investment property & rental yield FAQ

Which Australian city has the best rental yield in 2026?

Darwin has the highest gross rental yield of any Australian capital in 2026 at 6.0%, followed by Hobart (4.3%), Canberra (4.0%) and Melbourne (3.8%). Sydney has the lowest at 3.1%. Median dwelling values are from Cotality as at May 2026.

Is a high rental yield the same as the best investment?

No. Gross yield measures income only. Total return is yield plus capital growth, minus holding costs and the cost of your loan. High-yield cities like Darwin often have a less certain growth history, while low-yield cities like Sydney are priced for expected growth. The best investment depends on your strategy, not the single highest yield.

What is the difference between gross and net rental yield?

Gross yield is annual rent divided by property value, before costs. Net yield subtracts council rates, insurance, property management, maintenance, strata and vacancy, and is typically 1 to 2 percentage points lower. Net yield is the figure that reflects your real income before the mortgage.

How much rent do I need to cover an interest-only investment loan?

On the median Darwin dwelling (~$634,000, 6.0% yield) the implied gross rent of about $3,170 a month broadly covers the ~$2,660 interest-only cost on an 80% loan at 6.29%, before holding costs. On the median Sydney dwelling, the gross rent (~$3,315) falls well short of the ~$5,380 interest, leaving a gap the investor funds in exchange for expected growth. These are gross illustrations only.

Why does my borrowing capacity differ between lenders for an investment loan?

Lenders assess rental income, existing debts, living expenses and the assessment buffer differently, and many “shade” rental income to 75 to 80%. The same investor can be approved for very different amounts at different lenders, which is why comparing the market matters more for investors than for almost anyone else.

Should an investment loan be interest-only or principal and interest?

It depends on your cashflow, tax position and plans for the property. Interest-only keeps monthly costs lower and is common for investors, but usually carries a higher rate and a limited term, and doesn’t reduce the balance. Principal and interest builds equity faster. It’s a structure decision worth modelling, not a default.

How much does the interest rate really matter on an investment loan?

A great deal. On a $700,000 investment loan, a 0.40% rate difference is roughly $2,800 a year, deducted straight from your net return every year you hold. Over a typical hold period that compounds into tens of thousands, which is why investors compare lenders rather than accept their own bank’s offer.

Can I use the equity in my home to buy an investment property?

Often, yes. Many investors release equity from an existing property to fund the deposit on the next one. How it’s structured affects your tax position and your future borrowing, so it’s worth setting up correctly with a broker from the start. Lending is subject to approval.

What is rentvesting?

Rentvesting means renting where you want to live while buying an investment property in a market where the numbers stack up better. It’s a common strategy for buyers priced out of their preferred suburb who still want to own an appreciating asset.

Does a home loan or investment loan review with a broker cost anything?

No. Brokers like Everstone Finance are paid by the lender when a loan settles, so reviews, comparisons and borrowing-capacity assessments are free to you, with no obligation to proceed.

Do I need to be in Melbourne to work with Everstone Finance?

No. Everstone Finance is based in South Yarra and meets locally in person, but works with property investors across Melbourne and Australia-wide by phone and Zoom.

The bottom line: The yield chart tells you where the income is, Darwin on top, Sydney at the bottom, but not where the best investment is, because that depends on your strategy and the costs the chart ignores. The property delivers the yield and the growth; the financing decides how much of it you keep and whether you can do it again. That’s the part we make sure you win.

Know your numbers before you buy

We’ll tell you what you can borrow, at what rate, across 30+ lenders, and how to structure it for the property after this one. Honest, plain English, in writing.

Book an appointment